If you’ve studied economics like me, the name Hyman Minsky may be familiar. He was an American economist who developed the financial stability theory, basically saying that stability breeds instability. Think of a sand pile: at some point, adding one more grain, although infinitely small in itself, will make the pile crumble. That’s more or less what we’re witnessing right now for the sand pile called “Ev’s for all”, crumbling far quicker than even I had imagined. I wasn’t planning to return to the topic anytime soon but sometimes events force your hand, and there’s just too much that’s happened in the last weeks and months not to take note of, as it is kind of important for the whole car world.

The starting point as I remember it was sometime back in February when two things happened. Mercedes boss Ola Källenius, roughly at the same time as presenting the stupidest EV of them all this side of the Hummber EV, the electric G-class, came out and said that electrification of the whole Mercedes fleet would take longer than expected. That’s of course another way of saying that demand is lacking. Mercedes have pushed the date for the last combustion engine forward from 2030 to 2035, where it most certainly won’t stay.

Roughly at the same time, the FT ran an article on Lucid Motors, where Lucid boss Peter Rawlinson said that his company cannot rely on “bottomless wealth” from its 60% Saudi owners. In other words, the sheiks in the country of many sand piles are thinking of turning off the tap, if they haven’t done so already. Lucid has close to USD 5bn in the bank but is currently burning USD 1bn per quarter and lost close to USD 3bn in 2023. Given they’re not close to making a profit anytime soon, they will thus need to fundraise again before the end of the year to survive. In the current market, I wish them luck.

Luck is also what Rivian still needs, and this one hurts a bit more since I find it a really innovative company that have brought something new to the market, and have plans for continuing to do so in the future as well. A friend of mine drives the Rivian SUV and is thrilled about the car, its features and gadgets. However given a lack of Rivian car buyers, the company urgently needs to save money and announced in March that production has been paused in their new factory in Georgia and that instead, they will fall back on their old production plant which is cheaper to run. And whilst we’re on SUV’s, if anyone is curious about Fisker, they’re so close to the brink that they can go belly up at any point in time, and contrary to Rivian, the SUV called Ocean they’ve launched is crap in most testers’ view.

Moving on to the EV wannabes, Porsche is making all kinds of strange sounds around the all-electric new Macan. The idea was that the combustion one would be taken out of production in 2025-2026, and the all new E-Macan, launched as we speak, would then fully replace it. Now, the talk is of not replacing the ICE one until 2030. The issue for Porsche is that the new Macan is built as an EV from the first screw, meaning it’s not made for a combustion engine. Therefore, it’s most probably the old Macan that will be updated such as to live a bit longer. That’s certainly very far from what Porsche, blinded by the general EV trend, originally intended. It’s really terrible when client demand isn’t where you want it to be.

To round it all off, even the king of the hill Tesla has come down the hill, at least a bit. Firstly in stock price, where it’s down about 1/3 this year, making it by far the worst performer of the so called Magnificent Seven. That said, it’s still worth more than twice what Toyota is. Then there’s production numbers, where Tesla not only ships less cars than a year ago, but also produced around 70′ less cars in the first quarter than analysts were counting on. Tesla has also lost around 1/3 of its market share in the all-important Chinese market, falling from 10.5% to around 7% as per the Chinese Passenger Car Association, all due to the intense Chinese competition discussed in earlier posts.

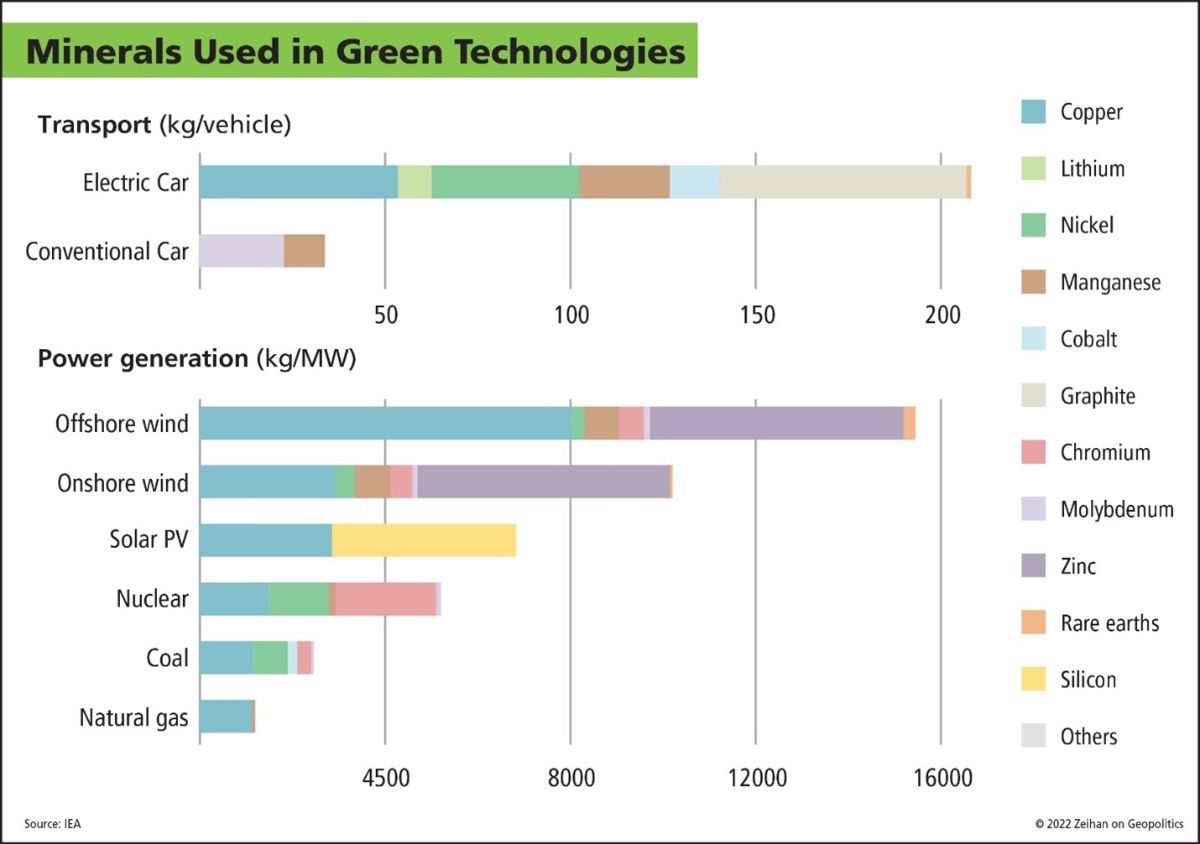

You’ll note that all of this has to do with falling client demand, and nothing has to do with the other fundamental EV issues, such as not even being close to having enough metals and related stuff to produce the EV’s our politicians plan for, and that the battery production with all its required input materials is both highly polluting and highly unethical. That comes on top of the waning demand, and as Ineos’ founder Jim Rathcliffe says, you can’t force EV’s down people’s throat – although I’m sure at least some politicians will try.

I yelled at European luxury automakers pathetic efforts to build competitive EV’s a few weeks ago, and also said the cheap part of the market risks being taken over by Chinese EV’s. That’s exactly what’s happening, and in addition, growth has stalled in the developed world for all the reasons we’ve already gone into. A challenging capital raising environment means that many of the new EV brands risk going under, and (especially European) politicians who are still incapable of delivering a charging network commensurate to the growth they want to see have done the rest. I’d say they should take most of the blame.

At the same time, I was surprised earlier this week to see the Biden Administration’s projection for what the US car market will look like in 2050. As can be seen above, EV’s aren’t expected to take over anytime soon, although they are projected to grow quite a lot. Hybrids continue to grow too, which we’ve been discussing here, and what for example Toyota has said all along. Most people drive short distances, and thus splitting a big battery pack in one car into five smaller packs in five cars makes most sense when materials are limited. Anyhow, by 2050, 2/3 of all cars are still expected to be what should be called combustion engine cars, since by then, I’m willing to bet we’ll have other stuff than fossil fuels to power combustion engines with, which also means they may be around for far longer than anticipated.

If you really want an EV, then as I’ve said before, there really is no better alternative than a Tesla, pretty much wherever you live. But if you don’t, be aware you’re part of a growing crowd and that your petrol car will be fine for years to come. As I was finishing this post, I saw the news that the European car safety organization Euro NCAP has come out with new rules, requiring a car’s essential functions to be handled by physical buttons, not over a screen, for a car to get the maximum five safety stars starting in 2026. Trying to sell a car in Europe that has less than five safety stars is all but impossible, so this will obviously cause further pain for many, especially most EV manufacturers. If we keep going at this pace, the future starts looking really bright!